Summary

Here, we present our recent findings on our Climate Action Tracker evaluation of net zero targets’ scope, architecture, and transparency. We have adapted extracts from Chapter 3.8 of our December 2023 Global Update.

- In our latest analysis of net zero targets, we find an increasing number of governments disclose plans on the type and scope of carbon dioxide removal within their borders to meet their longer-term targets — but detailed information across government’s plans remains scarce.

- Across 28 countries accountable for over 80% of global emissions, these plans aim for combined forest sinks of 4.7–5.7 GtCO2e, which would represent 12–15% of their 2019 emissions. Eight of these countries also plan for engineered carbon dioxide removals (such as direct air carbon capture) of 0.7–1.3 GtCO2e. With estimated costs for engineered CDR at a scale of up to USD 400 per tonne CO2, governments would need to invest hundreds of billions a year for these removals.

- Our findings point to the risk of over-relying on carbon dioxide removals to avoid the urgent need to make rapid deep cuts in emissions, prolonging the use of fossil fuels, and putting the 1.5˚C warming limit at risk.

Governments improved planning on carbon dioxide removal for net zero targets

As of May 2024, around 145 governments have announced – or are considering – net zero and carbon neutrality targets, covering close to 90% of global emissions. Among these are China’s 2060 carbon neutrality target, the EU’s 2050 net zero target, the US’s 2050 net zero target, and India’s 2070 net zero target.

During the early wave of net zero commitments, most were simply political declarations of intent, with details on what the net zero targets meant in practice largely missing. For instance, governments did not specify to what extent they planned to reduce emissions by the target year compared to “neutralising” them through carbon dioxide removals.

Many governments have now started to further substantiate their net zero targets by enshrining them into law or long-term strategies (LTS), and providing more details on their scope, ambition, and transition plans.

This blog outlines our recent findings on how governments have improved their current planning on carbon dioxide removal — sometimes known as ‘negative emissions’ — to meet their net zero targets, and why this matters.

What is carbon dioxide removal?

The IPCC Sixth Assessment Report (2022, page 1796) defines carbon dioxide removal (CDR) as “removing CO2 from the atmosphere and durably storing it in geological, terrestrial, or ocean reservoirs, or in products” for decades to millennia. Carbon dioxide removals can broadly be differentiated between several categories:

- Conventional CDR, such as forest sinks, capturing and storing carbon in land reservoirs.

- Engineered CDR includes other methods such as Direct Air Carbon Capture and Storage (DACCS) or Biomass Energy Carbon Capture and Storage (BECCS).

- Novel CDR based on sea or land, such as biochar and ocean alkalinisation.

Generally speaking, carbon dioxide removal technologies can face risks of reversibility (e.g., through forest fires) or face high costs and technological immaturity (e.g., around USD 270/tCO2 in 2022 for direct air carbon capture and storage, according to the 2023 The State of Carbon Dioxide Removal report).

As both Carbon Capture and Storage (CCS) and Carbon Capture and Utilisation (CCU) do not capture CO2 from the atmosphere, these concepts cannot be considered as a form of CDR, but rather an emissions reduction measure.

Why does carbon dioxide removal matter?

To halt global warming and meet the Paris Agreement’s 1.5°C temperature limit, first CO2 emissions and then greenhouse gas emissions need to be reduced to net zero or even negative levels.

Not all greenhouse gas emissions from agriculture and other activities can be reduced to zero, meaning that even if CO2 emissions can be reduced to zero or negative levels there will be a need for large scale negative CO2 emissions to counterbalance these residual greenhouse gas emissions.

This will only be feasible if the maximum possible emission reductions have been achieved for both CO2 and non–CO2 greenhouse gas emissions. However, even with the deepest reductions this may require hundreds of billions of tonnes of negative CO2 emissions in order to reach and maintain net-zero GHG emissions in the second half of this century.

Therefore, reaching net zero GHG emissions entails reducing emissions to the greatest extent possible, approaching zero emissions, and only then deploying carbon dioxide removal (CDR, or negative emissions) to compensate for residual GHG emissions, ultimately achieving net zero CO2 emissions by around 2050 and net zero GHG emissions by around 2070 at the global level according to the International Panel on Climate Change (2023, page 20).

While financial and policy support will be required to accelerate conventional, engineered and novel CDR deployment over time, governments seem to be prioritising a significant reliance on potentially available CDR instead of effectively reducing their own emissions.

Emission scenarios compatible with the 1.5°C Paris Agreement temperature limit show that global emissions need to become net negative as soon as possible. This mandates the accelerated scale-up of carbon dioxide removal (CDR) globally in parallel to rapid emission reductions as found in The State of Carbon Dioxide Removal report (2023) and UNEP Emissions Gap Report (2023, Chapter 7).

The reliance on CDR to limit global warming to 1.5°C, however, must be kept as low as possible, acknowledging the tremendous uncertainties around reliability, costs, and permanence.

How much do governments plan to rely on domestic carbon dioxide removal?

Despite recently updated long-term strategies and other policy planning documents, detailed information on governments’ plans to rely on CDR within their borders remains scarce. Of the 34 countries the Climate Action Tracker has assessed that have pledged net zero (as of May 2024), only 15 governments[1] provide more detailed information on LULUCF sinks and/or engineered CDR and storage in their net zero target year (see Table 1 further below).

Most of these governments plan to rely heavily on CDR or leave a share of their emissions out of their net zero target coverage. We conservatively estimate these residual emission to account for almost a fifth of their current emissions (excluding LULUCF emissions).

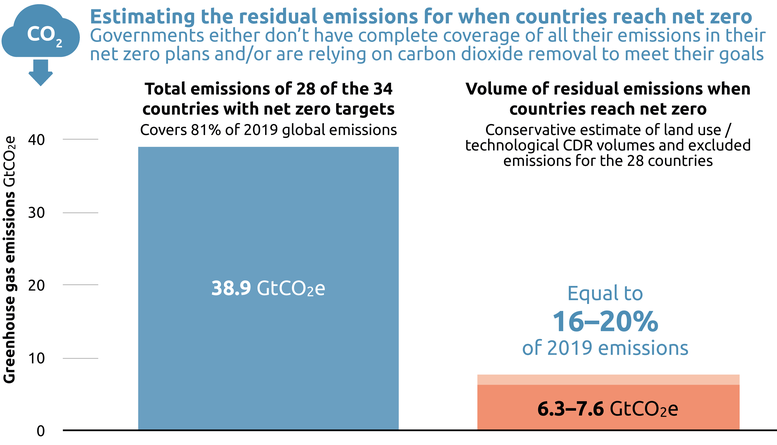

For this estimation, we took a closer look at 28 of the 34 governments with net-zero targets[2], which jointly cover 81% of global 2019 emissions.

Based on the latest available information, we estimate the remaining emissions in the respective net zero target years to amount to a minimum of 16–20% compared to 2019 emissions (see Figure 1, conservative estimate). This means that these 28 countries jointly only commit to reduce up to 80–84% of their emissions as part of their net-zero target, not 100%.

For example, Australia, Canada, Chile, New Zealand, Russia, Saudi Arabia and Viet Nam would still emit more than 30% of their 2019 emissions even after meeting their “net zero target”.

Governments are relying on forestry sinks (land use, land-use change and forestry, or LULUCF) in particular to balance remaining emissions.

As of May 2024, we estimate that the same 28 governments mentioned above jointly assume domestic LULUCF sinks of 4.7–5.7 GtCO2e, representing a combined 12–15% of their 2019 emissions.

Several governments transparently communicate their plans to rely on LULUCF sinks and/or engineered CDR underpinning their net zero targets, including Chile, Costa Rica, and South Korea. Alongside the need for transparency, countries should aim for a minimum reliance on LULUCF sinks and engineered CDR to meet their net zero target and underpin their targets with deep cuts in emissions across all sectors of the global economy.

Only eight governments currently communicate some information on domestic engineered CDR underpinning their net zero targets.[3] Their plans jointly amount to 0.7–1.3 GtCO2e, representing 5–10% of their 2019 emissions.

At estimated costs for engineered CDR at scale of up to USD 400 per tonne CO2 (see technology-specific estimates in The State of Carbon Dioxide Removal, 2023, page 18–19), governments will need to invest hundreds of billions a year for these removals.

These results for LULUCF sinks and engineered CDR are in line with other recently published literature in the field for different country samples, such as Smith et al. (2022), Buck et al. (2023), Mooldijk et al. (2023) and Smith et al. (2024).

Governments providing detailed information on LULUCF sinks and/or engineered CDR and storage in their net zero target year

| Country | Net-zero target | Domestic LULUCF sinks (planned in net-zero target year) |

Domestic engineered CDR (planned in net-zero target year) |

Removals outside of own border (planned in net-zero target year) |

|---|---|---|---|---|

| Australia | 2050 | 27 MtCO2e (5% of domestic 2019 emissions) |

38 MtCO2e (7% of domestic 2019 emissions) |

94 MtCO2e (17% of domestic 2019 emissions) |

| Canada | 2050 | 100 MtCO2e (13% of domestic 2019 emissions) |

0–201 MtCO2e (0–27% of domestic 2019 emissions) |

Not specified, reserves right to use reductions or removals outside own border in the future |

| Chile | 2050 | 65 MtCO2e (57% of domestic 2019 emissions) |

None identified | None identified |

| Costa Rica | 2050 | 6 MtCO2e (31% of 2019 emissions) |

None identified | None identified |

| EU27 | 2050 | 317–472 MtCO2e (9–13% of domestic 2019 emissions) |

281–606 MtCO2e (8–17% of domestic 2019 emissions) |

No use of reductions or removals outside own border to meet net-zero target |

| Germany | 2045 | 40 MtCO2e (5% of domestic 2019 emissions) |

None identified | Not specified, reserves right to use reductions or removals outside own border in the future |

| Indonesia | 2060 | 299 MtCO2e (31% of domestic 2019 emissions) |

None identified | None identified |

| Kazakhstan | 2060 | 45 MtCO2e (12% of domestic 2019 emissions) |

None identified | None identified |

| South Korea | 2050 | 25 MtCO2e (4% of domestic 2019 emissions) |

up to 7 MtCO2e (up to 1% of domestic 2019 emissions) |

No use of reductions or removals outside own border to meet net-zero target |

| Switzerland | 2050 | None identified | 5–7 MtCO2e (11–15% of domestic 2019 emissions) |

5 MtCO2e (11% of domestic 2019 emissions) |

| Thailand | 2065 | 120 MtCO2e (28% of domestic 2019 emissions) |

None identified | None identified |

| UAE | 2050 | 3.5 MtCO2e (2% of domestic 2019 emissions) |

9.5 MtCO2e (4% of domestic 2019 emissions) |

Not specified, reserves right to use reductions or removals outside own border in the future |

| UK | 2050 | 19 MtCO2e (4% of domestic 2019 emissions) |

70–80 MtCO2e (16–18% of domestic 2019 emissions) |

Not specified, reserves right to use reductions or removals outside own border in the future |

| USA | 2050 | 615–1471 MtCO2e (9–22% of domestic 2019 emissions) |

297–494 MtCO2e (5–8% of domestic 2019 emissions) |

Not specified, reserves right to use reductions or removals outside own border in the future |

| Viet Nam | 2050 | 185 MtCO2e (41% of domestic 2019 emissions) |

None identified | None identified |

Key challenges with carbon dioxide removal

The different types of CDR face uncertainties in terms of permanence, sustainability, and availability, putting governments’ current planning on the pace, scale, and costs of deploying CDR as part of their net zero strategies into question.

Conventional CDR, such as forest sinks in particular, face issues of both permanence and scarcity. Climate change and direct human interference lead to uncertainty on the performance of stored carbon in forests and other ecosystems, according to the 2023 UNEP Emissions Gap Report (Chapter 7). For instance, forest fires release stored carbon into the atmosphere, negating any climate benefit of storing the carbon in the first place.

There is limited land available for carbon dioxide removals from forest sinks. The Land Gap Report (2023) found that combined government climate pledges, including their NDCs and LTSs, propose one billion hectares of land prioritised for conventional CDR — more than the combined areas of South Africa, India, Türkiye and the European Union. These plans exceed the global sustainable potential for conventional CDR.

Engineered CDR such as Direct Air Carbon Capture and Storage (DACCS) or Biomass Energy Carbon Capture and Storage (BECCS) face challenges in relation to financial cost, limitations on biomass availability (in the case of BECCs), scalability and access to sufficient and appropriate geological storage as presented in the 2023 State of Carbon Dioxide Removal report (2023, page 18–19).

Novel CDR based on sea or land such as biochar and ocean alkalinisation face various challenges including environmental hazards and unwanted side effects, financial and technological viability, and legal issues. Further research on the environmental challenges surrounding these approaches is needed and much further research will be needed to fully understand these approaches.

Recommendations to governments on carbon dioxide removal

As governments further develop their planning around CDR as part of their net zero and other long-term targets, we have identified key aspects to consider. Governments need to:

- Focus their attention on reducing their own emission towards real zero as part of their net zero targets, and

- Accelerate research on the deployment, scalability, and environmental sustainability of engineered CDR and novel CDR based on sea or land to achieve net negative emissions in the second half of this century, and

- Begin early scale deployment of small-scale engineered CDR to test feasibility, scalability, and environmental consequences, and

- Advance their planning on how and to what degree they intend to rely on CDR as part of their net zero and other long-term strategies, and

- Transparently communicate and differentiate between conventional, engineered and novel CDR based on sea or land in target-setting and progress reporting.

The Climate Action Tracker will continuously track and assess governments’ plans going forward to allow for a better understanding of their individual and joint planning.

Endnotes

[1] This count includes the European Union (EU27).

[2] Australia, Brazil, Canada, Chile, China, Colombia, Costa Rica, European Union, Germany (analyzed separately but not aggregated as included in EU), India, Indonesia, Japan, Kazakhstan, Nepal, New Zealand, Nigeria, Russia, Saudi Arabia, Singapore, South Africa, South Korea, Switzerland, Thailand, Türkiye, UAE, UK, US, and Viet Nam. We excluded six countries (Argentina, Bhutan, Ethiopia, Morocco, Peru, The Gambia) because we do not have enough information from the governments to quantify their net zero targets.

[3] Australia, Canada, EU, Germany, South Korea, Switzerland, UK, and the US.

Source link : View Article